Financial Freedom Blueprint: A Step-by-Step System for Building Wealth at Any Income Level

Financial independence isn’t reserved for the wealthy or well-connected. With systematic planning and consistent execution, people at virtually any income level can build significant financial security over time. This comprehensive guide outlines a step-by-step approach to achieving financial freedom, focusing on practical strategies that work regardless of your starting point.

Understanding True Financial Freedom

Financial freedom means different things to different people, but at its core, it represents having enough resources to make life choices without being overly constrained by financial factors. This doesn’t necessarily mean extravagant wealth, but rather:

- Freedom from debilitating financial stress

- Ability to weather financial emergencies without derailing your life

- Option to make career and life decisions based on personal values rather than solely on income

- Capacity to support important personal goals and meaningful pursuits

Phase 1: Building Your Financial Foundation (Months 1-6)

Before focusing on wealth-building, establishing a solid financial foundation is essential.

Step 1: Create Clarity Through Financial Mapping

You can’t improve what you don’t measure. Begin by documenting your current financial reality:

- Net worth statement: List all assets (what you own) and liabilities (what you owe)

- Cash flow tracking: Monitor all income and expenses for at least 30 days

- Debt inventory: Document all debts including balances, interest rates, and minimum payments

- Financial obligations map: Outline recurring financial commitments and their importance

This clarity enables informed decision-making and prevents the “financial fog” that leads to poor choices.

Step 2: Establish Your Financial Operating System

Implement a reliable system to manage day-to-day finances:

- Banking structure: Set up appropriate checking and savings accounts (consider high-yield options)

- Bill payment system: Automate essential bills to prevent missed payments

- Spending methodology: Choose between cash envelopes, prepaid cards, or dedicated accounts for discretionary spending

- Tracking mechanism: Select manual or automated expense tracking solutions

The best system is one you’ll actually use consistently—prioritize simplicity and sustainability over complexity.

Step 3: Build Initial Emergency Reserves

Financial security begins with a buffer against life’s inevitable surprises:

- Starter emergency fund: Accumulate $1,000-2,000 as quickly as possible

- Designated account: Keep these funds in a separate, accessible savings account

- Clear parameters: Define what constitutes a genuine emergency (unexpected, necessary, urgent)

- Rapid rebuilding plan: Create a strategy to immediately replenish funds if used

Even a modest emergency fund dramatically reduces financial stress and prevents minor setbacks from escalating into financial crises.

Phase 2: Debt Elimination and Protection (Months 7-24)

With basic systems in place, focus on eliminating obstacles to wealth-building.

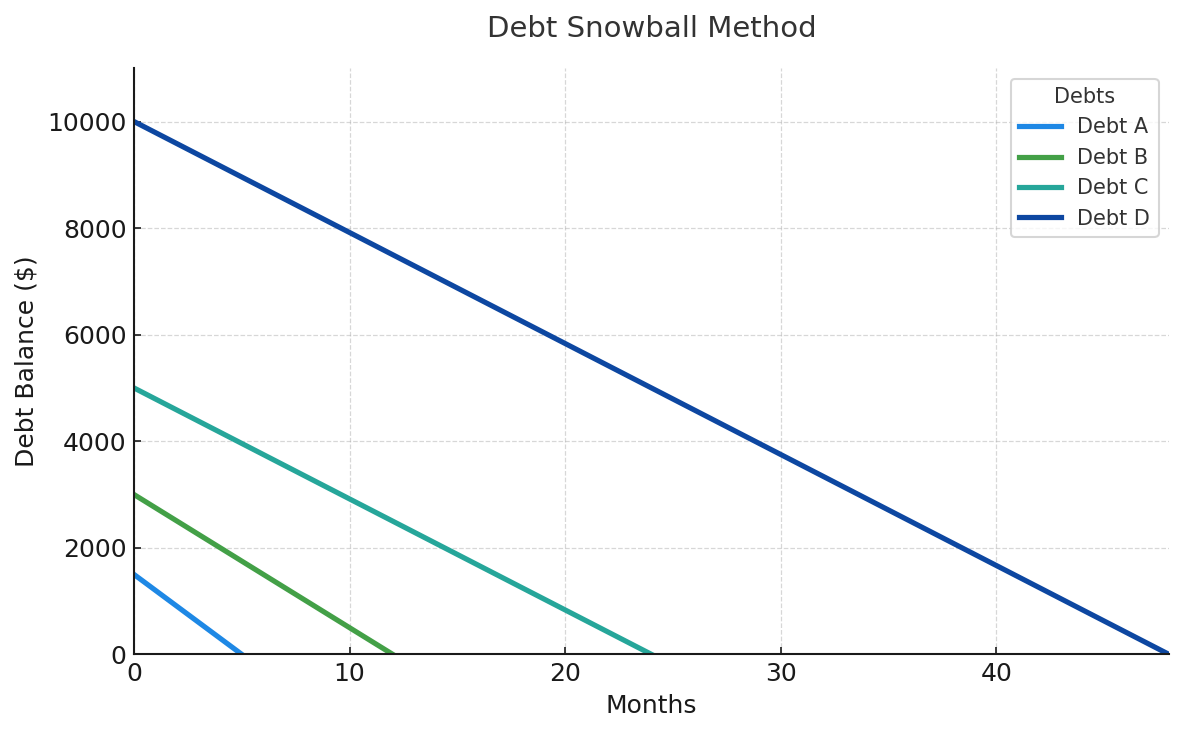

Step 4: Implement Strategic Debt Elimination

Consumer debt represents one of the biggest obstacles to building wealth:

- Debt prioritization: Choose either highest-interest method (mathematical advantage) or smallest-balance method (psychological advantage)

- Payment acceleration: Apply all available extra funds to the priority debt

- Snowball momentum: As each debt is eliminated, roll payments to the next priority

- Debt payoff timeline: Create a visual representation of your projected debt-free date

Focus most intensely on high-interest consumer debt (credit cards, personal loans). Student loans, mortgages, and other lower-interest debts can be addressed with a longer-term strategy.

Step 5: Establish Comprehensive Protection

Protect your financial progress against major life disruptions:

- Full emergency fund: Expand reserves to cover 3-6 months of essential expenses

- Insurance audit: Ensure appropriate coverage for health, auto, home/rental, and liability

- Income protection: Consider disability insurance, especially for single-income households

- Basic estate documents: Create a will, advance healthcare directive, and power of attorney

Without adequate protection, a single emergency can erase years of financial progress.

Phase 3: Accelerated Wealth Building (Years 2-10)

With debt eliminated and protection in place, wealth building begins in earnest.

Step 6: Optimize Income Potential

Increasing income provides more resources for wealth building:

- Primary career enhancement: Strategic upskilling, certification, or education for advancement

- Secondary income development: Side businesses, freelancing, or part-time work aligned with skills

- Passive income cultivation: Investments in income-producing assets (dividend stocks, rental property)

- Income acceleration plan: Specific 3-year plan for increasing total household income

Even modest income increases, when consistently invested, dramatically impact long-term wealth.

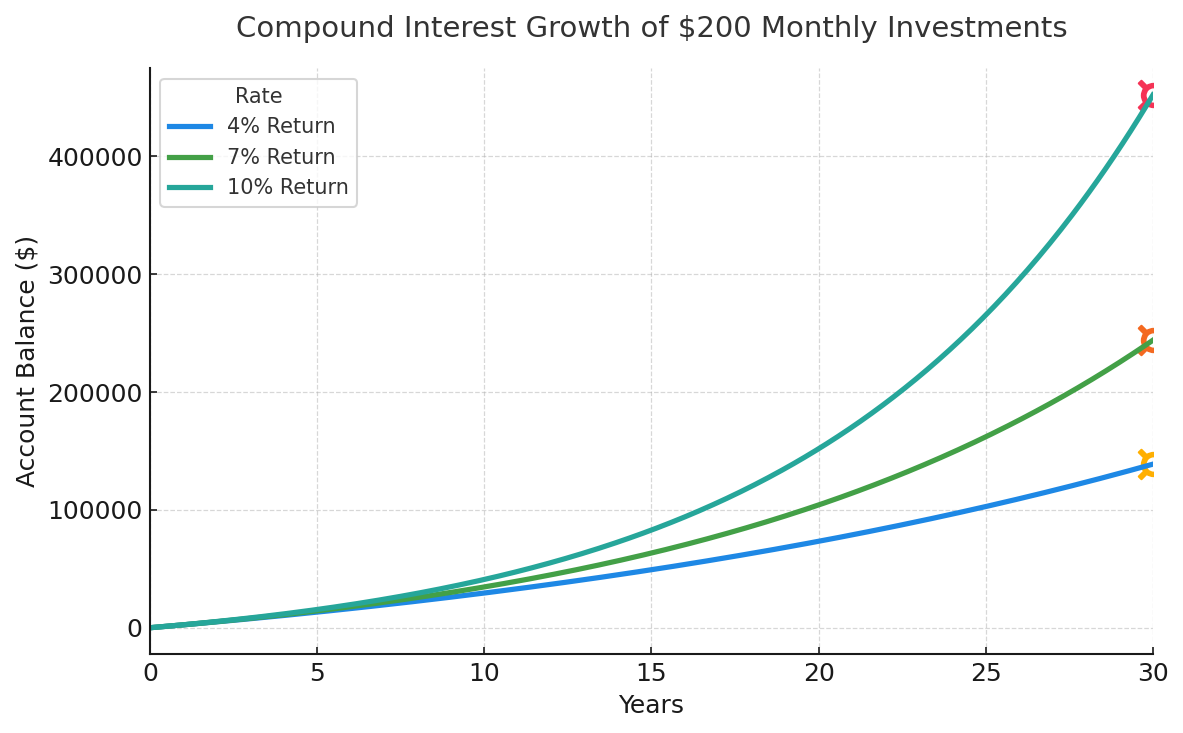

Step 7: Implement Strategic Retirement Investing

Retirement investing forms the core of most wealth-building plans:

- Employer plan optimization: Contribute at least enough to capture full employer matching

- Tax-advantaged account maximization: Utilize IRAs, HSAs, and other tax-preferred vehicles

- Investment simplification: Consider target-date funds or simple index portfolios for easy implementation

- Contribution automation: Set up automatic transfers to ensure consistent investing

The combination of tax advantages, compound growth, and systematic investing makes retirement accounts the foundation of most wealth-building strategies.

Step 8: Develop Tax Efficiency

Strategic tax planning prevents unnecessarily surrendering wealth:

- Income tax optimization: Maximize appropriate deductions and credits

- Account location strategy: Place investments in appropriate accounts based on tax treatment

- Tax-loss harvesting: Strategically realize losses to offset gains in taxable accounts

- State tax consideration: Evaluate state tax implications for major financial decisions

The difference between poor and optimal tax planning can easily represent hundreds of thousands of dollars over a lifetime.

Phase 4: Lifestyle Design and Financial Independence (Years 10+)

As wealth accumulates, focus shifts to optimizing life satisfaction and legacy.

Step 9: Create a Fulfillment-Based Lifestyle Design

Align financial resources with maximum life satisfaction:

- Values-based spending audit: Analyze which expenditures provide genuine fulfillment

- Intentional lifestyle design: Reallocate resources toward high-fulfillment activities

- Work integration evaluation: Consider changes to work structure (reduced hours, sabbaticals, career change)

- Geographic arbitrage exploration: Evaluate whether relocation could improve financial position and lifestyle quality

Research consistently shows that beyond meeting basic needs, happiness comes more from how money is used than how much is accumulated.

Step 10: Implement Advanced Wealth Optimization

Fine-tune wealth strategy for maximum efficiency:

- Investment efficiency analysis: Review and minimize investment expenses and tax drag

- Withdrawal strategy development: Plan optimal account sequencing for retirement distributions

- Healthcare funding plan: Specifically address future healthcare costs in financial projections

- Longevity protection: Consider strategies to mitigate longevity risk (outliving resources)

Step 11: Establish Legacy and Estate Structure

Prepare for the ultimate distribution of your resources:

- Comprehensive estate planning: Work with qualified professionals for appropriate documentation

- Legacy vision development: Define how you wish to impact family and community

- Charitable strategy integration: Implement efficient giving mechanisms for causes you support

- Family financial education: Prepare heirs for responsible financial management

Core Implementation Principles

Across all phases, these principles maximize success probability:

Consistency Over Intensity

Financial success resembles a marathon more than a sprint. Moderate, sustainable actions maintained over time outperform brief periods of intense financial focus followed by neglect.

Automation and Systematization

Remove willpower from the equation by automating positive financial behaviors:

- Automatic bill payments

- Scheduled transfers to savings and investments

- Systematic investment plans

- Calendar-based financial reviews

Progress Monitoring

Regular review prevents drift and maintains motivation:

- Weekly spending check-ins (15 minutes)

- Monthly financial reviews (30 minutes)

- Quarterly progress assessments (1 hour)

- Annual financial planning sessions (3-4 hours)

Continual Education

The financial landscape constantly evolves, making ongoing learning essential:

- Read one personal finance book quarterly

- Follow reputable financial websites and podcasts

- Consider working with a fee-only financial planner for occasional guidance

- Participate in communities focused on financial improvement

Conclusion: The Compound Effect of Financial Discipline

Financial freedom results from the compound effect of consistently sound decisions over time. The most powerful wealth-building tool isn’t a sophisticated investment strategy or obscure tax loophole—it’s the disciplined application of fundamental principles.

By methodically progressing through these phases, you create not just financial resources, but expanded life options. The ultimate purpose of building wealth isn’t the money itself, but the freedom it provides to live according to your values and priorities.

The journey to financial freedom isn’t always easy, but with systematic implementation of these principles, it’s achievable regardless of your starting point. The best time to begin was years ago—the second-best time is today.